Foreclosure Defense for DC & Maryland Homeowners

Foreclosure notices in D.C. and Maryland can move fast; sometimes, it’s a matter of weeks.

Get help from a foreclosure defense lawyer in Maryland or Washington, DC. They might stop the process using laws like the Real Estate Settlement Procedures Act, DC’s Home Loan Protection Act, DC’s Consumer Protection Procedures Act, DC’s Deed of Trust Act, Maryland’s Consumer Protection Act, or Maryland’s Consumer Debt Collection Practices Act.

Request a free consultation

Common foreclosure issues in DC and Maryland

How a Maryland & DC foreclosure defense lawyer can stop the sale

Two Paths in D.C.: Most lenders today use the judicial track. This means they file a foreclosure case in D.C. Superior Court, and you get a chance to defend the case in court (with strict response deadlines). The info below covers the nonjudicial track (power-of-sale) that requires foreclosure mediation first.

If You Miss a Mortgage Payment (Nonjudicial Track)

Notice of Default: Your lender must mail a Notice of Default that includes your right to request foreclosure mediation.

30-Day Deadline: You generally have 30 days from the lender’s mailing of that notice to request mediation.

Why It Matters: If you request mediation on time, the lender cannot hold a trustee’s sale until mediation finishes and a Final Mediation Certificate is issued and recorded. (A sale without a recorded Final Mediation Certificate can be void.)

What Happens Next: After mediation (if no agreement), the lender can continue toward foreclosure by recording the certificate and giving formal sale notice.

Tip: Whether your case is judicial or nonjudicial, timing is critical. Talk with a D.C. foreclosure defense lawyer as early as possible, ideally before mediation in the non-judicial track or right after you’re served with a court complaint in the judicial track. Doing so will help you use all defenses and options you have available.

This is general information, not legal advice.

In Maryland, there can be two opportunities for mediation. One is before foreclosure is filed. This is known as “pre-file” mediation. The other is after foreclosure is filed. This is referred to as “post-file” mediation.

Before foreclosure is filed: Your lender will likely send you a Notice of Intent to Foreclose. This notice must have a Preliminary Loss Mitigation Affidavit. It should outline loss mitigation options. Also, it should explain how to request pre-file mediation. This can help you resolve the default before the lender files for foreclosure. If you decide to do pre-file mediation, the foreclosure can’t proceed until it is resolved. To have a post-file mediation, your pre-file mediation agreement must include this right.

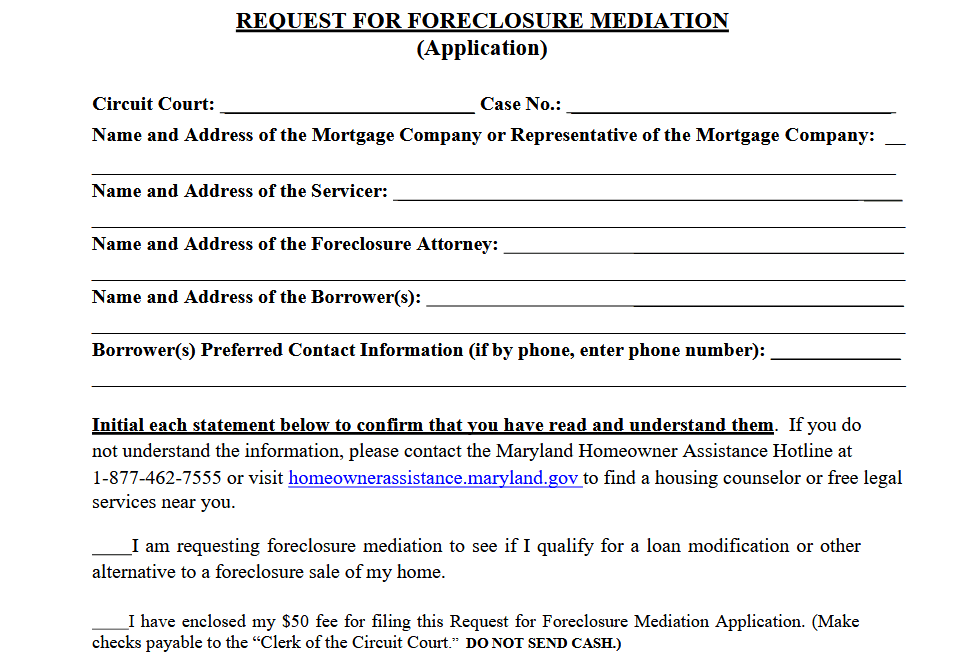

After foreclosure is filed: If you didn’t fix things before this, your lender will likely file an Order to Docket. This may also be called a “Complaint to Foreclose” or “Notice of Foreclosure Action.” The lender will send you a Final Loss Mitigation Affidavit. You’ll also get a Request for Foreclosure Mediation form. If the Order to Docket contained something called a “Final Loss Mitigation Affidavit,” you likely have only 25 days to complete the form and file it with the Circuit Court. Filing this form costs $50.

Important: Once mediation is done, the foreclosure can proceed quickly. If you’re facing foreclosure, talk to a lawyer right away—ideally before mediation.

This is general information, not legal advice.

It’s your home.

They’re your rights.

We’ll help you protect both.

Their mistake shouldn’t cost you your home

Life happens. Sometimes you lose a job, get sick, or just need a break to catch up.

Many homeowners sought forbearance or loan modifications for help. But the mortgage company made things worse. Maybe they didn’t explain how payments would work once forbearance ended. They might have promised a loan modification but then broke that promise. Or they could have said you were behind on payments when you actually weren’t.

Sometimes, it’s just the mortgage company’s mistake. They might misapply payments, add surprise fees, or send confusing statements. This can lead you toward foreclosure, even if you did everything right.

Whatever brought you here, foreclosure shouldn’t be the last word. If the servicer broke the rules, lied, or mishandled your account, you have solid legal choices. You can fight back, fix the mess, and protect your home.

How foreclosures happens. Here’s why it may not be your fault

Mortgage companies are supposed to help you find ways to stay in your home, but too often they make it harder.

Forbearance plans often lack clear guidance on payment after they end. Loan modifications get delayed, mishandled, or mysteriously denied. Sometimes it’s just messy: late payments, escrow errors, fake fees, or missing documents.

It all adds up and homeowners end up with default notices they shouldn’t have gotten.

When you’re buried in paperwork, moved around departments, or looking for clear answers, it’s easy to feel like it’s your fault. But the truth is: the system is rigged to push you out faster than it should.

How we fight back and protect your home

We dig deep. We demand your servicing history. We check the numbers. And we hold servicers accountable for breaking laws like RESPA and TILA.

If they violated loss mitigation laws, lied about loan mods, double-tracked foreclosure, or padded your balance with junk fees, we make them prove it. When they can’t, you may have the leverage to stop the foreclosure or strike a better deal.

Sometimes, we discover counterclaims that change the power dynamic. This can give you real bargaining power. You can fix the loan, stay in your home, and move on with your life.